Investors have plenty to feel positive about. Inflation is easing, with the latest data showing an annualized rate of 2.4%, just shy of the Fed’s target by less than half a percentage point. Meanwhile, the stock market continues its bullish run, with the S&P 500 hitting a record high of 5,822 on Friday, marking a 22% year-to-date gain.

The naysayers have, so far, been proven wrong – the economy, at least as far as the stock market is concerned, remains robust. Oppenheimer’s chief investment strategist, John Stoltzfus, echoes this positive sentiment, stating, “The S&P 500’s closing price suggests to us a bull market that persists bolstered by economic resilience supported by business and consumer activity with opportunity for stocks to move higher into year-end… We remain positive on equities.”

How positive is Oppenheimer when it comes to equities? Positive enough for the firm’s analysts to project massive gains for certain stocks – including one with a potential upside of up to 740%.

We’ve dived into the TipRanks database to gauge Wall Street’s general view on two Oppenheimer picks. The consensus? Strong Buy ratings across the board, with substantial upside potential. Let’s take a closer look at the details.

Rani Therapeutics (RANI)

Biologics made serious waves in the medical world. These are a class of drugs that target severe and chronic autoimmune, inflammatory, and metabolic diseases – conditions that have in the past proven resistant to traditional treatments and medications. The big problem with biologics is the delivery – they are dosed through IV infusion, as they cannot withstand stomach acids. This is where Rani Therapeutics, the first Oppenheimer pick we’ll look at, has made its great contribution.

The company has developed the RaniPill, a delivery system that allows biologic drugs to be dosed orally. The RaniPill capsule can move through the stomach and remain intact, allowing for the biologic drug within to be effectively absorbed by the highly vascularized wall of the small intestine. It’s an innovative design that bypasses one of the largest ‘patient problems’ with biologics, improving both patient comfort and medication compliance.

Rani has followed up the development of this new delivery system with several clinical trials on new drug candidates targeting several applicable metabolic or inflammatory conditions. Key drugs in its pipeline include RT-102 for osteoporosis and RT-111 for psoriasis, both of which have shown promising results in early trials. RT-102 is slated to begin a Phase 2 trial in Europe by year-end, while RT-111, following positive Phase 1 results, will be tested at higher doses to further assess safety and efficacy.

In addition, the company is working with ProGen on the development and commercialization of PG-102, an obesity treatment, delivered with the RaniPill and designated RT-114. Development is focusing on convenient delivery through a once-weekly dose, and a Phase 1 study is planned for initiation next year.

Oppenheimer analyst Andreas Argyrides sees great potential in Rani’s pipeline, noting that it could open the door to the global biologics market, which was valued at $516 billion in 2022 and is projected to reach $856 billion by 2031. Argyrides estimates that Rani’s pipeline could generate $1.1 billion in total product revenue.

“We consider Rani Therapeutics a compelling investment opportunity based on its innovative RaniPill… The RaniPill’s ability to achieve bioavailability comparable to or better than subcutaneous injections while eliminating the discomfort and inconvenience associated with needle-based delivery positions it as a potential game-changer in the biologics market across multiple indications,” Argyrides opined.

Discussing both the stock and the clinical pipeline, the analyst adds, “While shares have been under pressure so far this year due to a lack of catalysts, we see an opportunity for the stock to recover with the initiation of a Ph2 study with RT-102 in osteoporosis in Europe this year followed by an IND in the US. Positive Phase 1 results from RT-111 in psoriasis and from ProGen’s PG-102 hint at the potential to address significant unmet needs across various therapeutic areas, including metabolic and inflammatory diseases. With strong IP covering the RaniPill, RaniPill HC and the delivery of various biologics and large molecules using the platform, we see Rani as a pioneer in the oral biologics space and we recommend buying shares at current discounted levels.”

Backing this positive outlook, Argyrides gives RANI a Buy rating, with a $17 price target, implying a robust one-year upside potential of ~740%. (To watch Ahmad’s track record, click here)

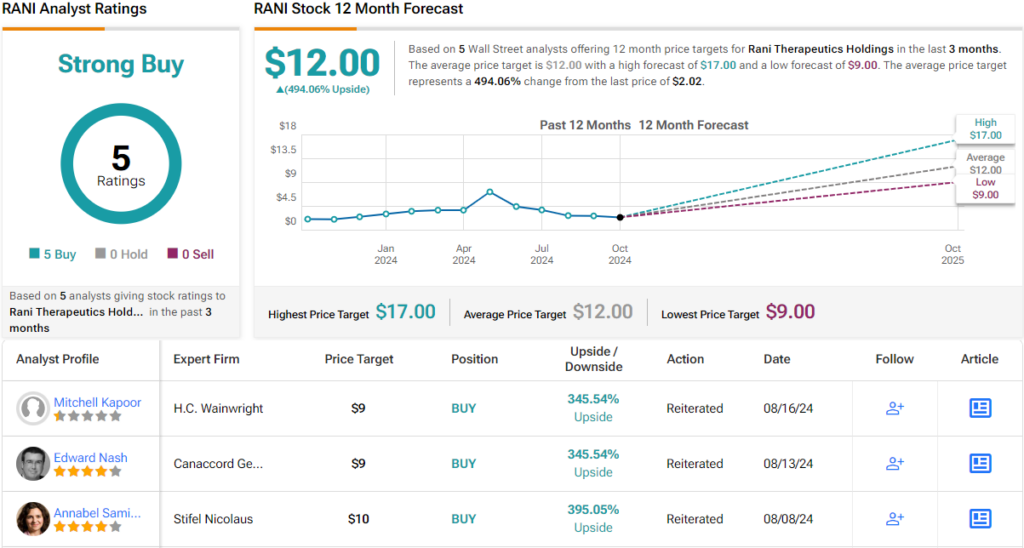

Overall, RANI has picked up 5 recent positive analyst reviews, for a unanimous Strong Buy consensus rating. The shares are trading in the penny-stock range, at $2.02, and the $12 average price target implies a one-year upside potential of 494%. (See RANI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.